Growth Scare Hits Risk Assets. High valuations come with high expectations. U.S. equity markets step back on growth concerns.

Market Update

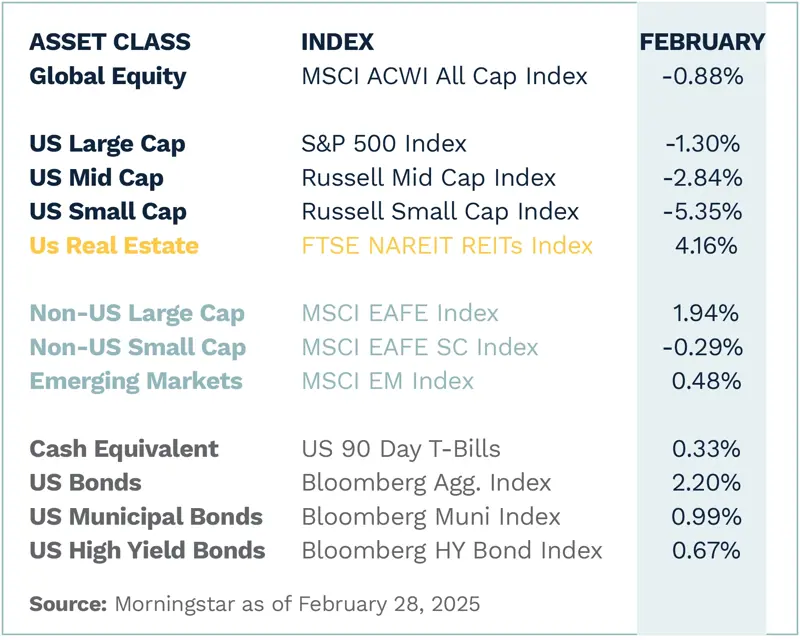

KEY OBSERVATIONS

Growth Scare Hits Risk Assets – Weaker economic data, a patient Fed and shifting policy dynamics fueled slowdown fears triggering a broad selloff of U.S. equities, with defensive sectors outperforming.

Growth Puts Spotlight on Valuations – High-valuation stocks fell more than peers, while value and defensive sectors led. Consumer staples outperformed consumer discretionary by 11%, while Treasuries rallied amid shifting markets sentiment.

International Extends its Lead – The MSCI EAFE Index, a proxy for non-U.S. developed equity exposure, took another step forward and added to its 2025 lead over the S&P 500, led by EU financial and defense spending along with a cooling of U.S. high valuation stocks.

RECAP

Global equity performance was flat to negative while fixed income performance was generally positive in February as tariffs dominated news headlines. U.S. equities underperformed non-U.S. developed and emerging market equities. Historical Fed minutes, released with a five-year lag, reveal that policymakers in 2018 and 2019 prospectively discussed the economic impact from the Trump tariff policies when considering monetary policy. This latest decision aligns with our view that inflation risks remain elevated, reinforcing our portfolio positioning for 2025 and beyond.

Shifting policy dynamics, a patient Federal Reserve holding rates steady and weaker economic data have left markets questioning the strength of future growth. These concerns were amplified when the Atlanta Fed’s GDPNow estimate turned negative for the first time since 2022. While the estimate may have been skewed by a rush of inventory builds in January ahead of the new administration and potential tariffs (remember import spend negatively impacts GDP), it still unsettled investors. Further fueling anxiety, real consumer spending fell by -0.5%, and consumer sentiment posted its sharpest decline since August 2021, dropping from 105.3 to 98.3. Investor sentiment quickly turned negative, triggering a broad selloff in February across many risk assets.

A slowdown in U.S. growth raises questions about the lofty valuations currently assigned to equities. Markets reflected this shift, as stocks and sectors “priced for perfection” suffered steeper declines than their lower-valuation peers. As a result, defensive sectors and assets outperformed. Value stocks led growth stocks and defensive sectors outpaced speculative ones, most notably seen in the nearly 11% performance gap between consumer staples (defensive) and consumer discretionary (speculative).

The Magnificent 7 pulled back sharply, with Tesla leading the decline, down nearly 30% for the month. Bitcoin, an asset we often view as a proxy for investor risk appetite, fell nearly 20% from recent all-time highs. In fixed income, Treasuries rallied, particularly long-duration assets. The 10-year yield, which was approaching 5% not long ago, is now closing in on 4%.

LOOKING AHEAD

Only a few days into March and the Trump bump has fizzled. This is perhaps most evidenced by the divergence in global stock prices with non-U.S. equity markets pushing higher while domestic equities drift lower amid a weaker dollar and waning economic data. Fortunately, a globally diversified approach across asset classes has held up as expected with traditional fixed income offering meaningful support. Moreover, the fundamental underpinnings remain quite good. In fact, the S&P 500 reported growth in earnings of 17.8% in the most recent quarter, its highest growth rate in 4 years. The change in sentiment is undeniable as investors have grown increasingly impatient with the vacillating policy direction of the administration. Yet despite all of this growing consternation, the market is in largely the same place it was before the election. Episodes of market weakness can offer investors important insights into their own tolerance for risk. We would be happy to revisit your financial plan to make sure it remains in alignment with your future goals.