Fed transition underway. Kevin Warsh assumes the role of Fed Chair with growth and inflation trending in opposite directions.

KEY OBSERVATIONS

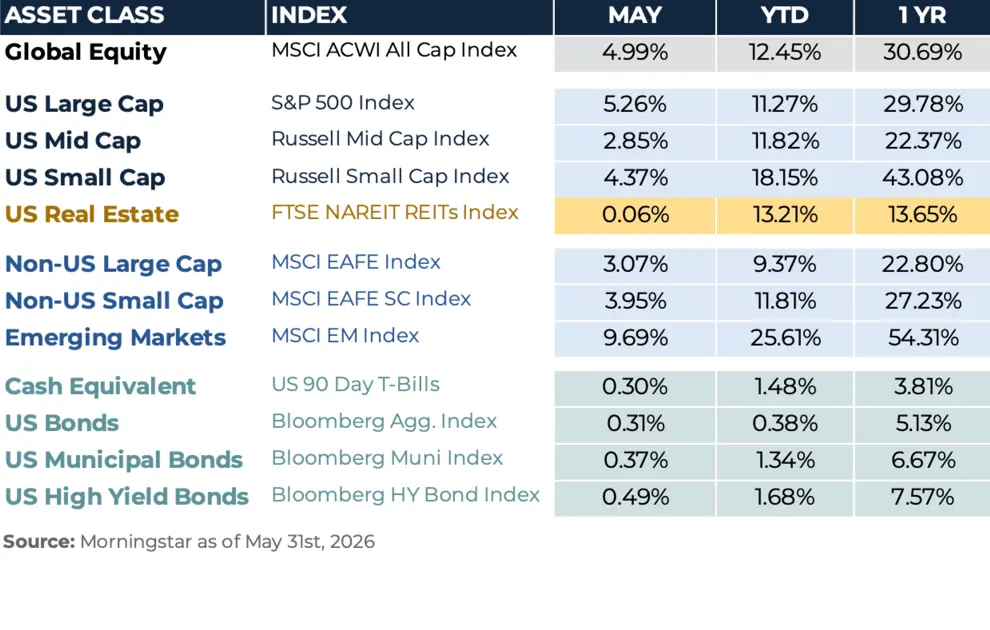

Equity markets push into record territory – Global equities continued to push higher in May, bolstered by strong Q1 corporate earnings and an acceleration in enthusiasm surrounding AI.

Emerging Markets lead the way – On the back of strong gains in Korea and Taiwan, emerging market paced the advance for global equity markets.

Musical chairs – Kevin Warsh assumed his role as Fed Chair in May. He steps into the role at a very difficult time for monetary policy. Going forward, the Fed will need to contend with a softening labor market and a concerning resurgence of inflation that is further complicated by ongoing geopolitical risks.

RECAP

May extended the global equity rally as markets grew increasingly optimistic about a potential diplomatic breakthrough between the U.S. and Iran, and blockbuster technology earnings pushed major indices to fresh all-time highs. Although inflation data reminded investors that price pressures remain stubbornly persistent, risk appetite held firm as markets looked past near-term headwinds and focused on strong corporate fundamentals and the prospect of easing geopolitical risk.

Large cap U.S. equities continued their advance. The S&P 500 Index returned nearly 5.3% for the month, closing at a new record above 7,500, with the Nasdaq gaining more than 8%. Technology stocks were the dominant force as enthusiasm around the AI trade accelerated. Nvidia reported 85% year-over-year revenue growth, and shares of Dell surged over 30% on a strong earnings beat, reinforcing the broadening of the AI infrastructure narrative beyond chipmakers and into the full technology stack. Smaller companies also participated in the market advance, though at a more measured pace. The Russell 2000 Index gained 4.4% and achieved a new all-time high, supported by a decline in Treasury yields and continued broadening of earnings growth into cyclical sectors like industrials and materials.

International equities also posted solid gains but trailed their U.S. counterparts. The MSCI EAFE Index returned 3.1%, with broad participation across both Europe and Japan. Emerging markets continued to stand out. The MSCI EM Index surged 9.7%, driven by continued strength in semiconductors and AI-related names across Taiwan and South Korea. EM equities are now up more than 25% year to date and more than 50% over the past year.

Fixed income returns were more muted, with the Bloomberg U.S. Aggregate Bond Index posting a 0.3% gain. Bond yields initially edged lower as geopolitical uncertainty weighed on growth expectations, but reversed course later in the month due to hotter-than-expected inflation data. Kevin Warsh officially assumed the role of Fed Chair in May, marking a leadership transition that markets will closely monitor. Warsh was sworn in at a difficult time for the Fed. April's PCE reading (the Fed’s preferred measure of inflation) came in at 3.8% year-over-year, its highest level since mid-2023, and Q1 GDP growth was revised down to 1.6% from the initial 2.0% estimate. Against this backdrop, the April FOMC meeting minutes revealed the most internal dissent since 1992, with a majority of officials warning that rate hikes could become necessary if inflation continues to run above the 2% target.

OUTLOOK

Equity performance in May was buoyed by accelerating enthusiasm for all things “Artificial Intelligence”, and the much-anticipated IPOs of companies like SpaceX, Anthropic and OpenAI will only serve to fan the flames. The recent rally in equity markets is supported by notably strong earnings growth, but longer-term stability will be dependent upon how effectively companies can translate AI investment into tangible improvements in earnings and profitability. The fervor with which equity markets continue to push forward runs counter to some of the uncertainties emerging within the bond market, where a combination of stubborn inflation and persistently elevated budget deficits have put upward pressure on bond yields. Markets will be heavily focused on how the Fed responds to the increasingly complicated macro backdrop, while the approach of the mid-term elections could add another layer of uncertainty. Even so, we would be cautious about allowing political noise to overshadow the broader fundamental picture. With bond yields well above 4% in the U.S., the higher cushion from coupons is favorable and helps insulate portfolios against modest increases in interest rates. We remain convicted that a balanced approach is crucial in the current environment. The excitement surrounding AI has fostered an element of short-termism and led to a market that is easily influenced by rapidly evolving narratives, which increases the risk of behavioral mistakes. We continue to favor an approach that is driven by the long-term fundamental drivers of return while remaining cognizant of evolving near-term risks.